Key Takeaway: Risk Classification and Management

“Risk is part of venture but it can be tackled and it should be tackled.”

Introduction

Most activities have risks associated with them because there is always a possibility of failure. The activities that result in a financial loss for which one is not prepared nor has reserves are very dangerous because it requires immediate unplanned expenses which may put an end to the venture. Although different industries have classified risk as per their relevance, risks are usually speculative and pure. Speculative risk is where the venture may result in either a profit or loss such as buying a lottery ticket and pure risk is where it shall definitely result in a loss such as a motor accident.

What it means by risk being a part of a venture is that whether it is an individual going to work, providing professional service, performing physical labor or intellectual due diligence, or an organization expanding its business, products, and services, they both have the chance of failures either by accident, negligence or fraud. Such failures result in financial loss which shall impact the profit and loss accounts severely or may even end the venture.

Today we are surrounded by numerous risks that may vary from accidental damage to appliances, loss of devices, data leaks, loss of access or control of assets and functionalities, and accidental losses due to fire and natural events. Organizations also have similar and complex risks. These risks can be classified into personal, property & assets, and liability. These risks can be tackled by eliminating, consuming, or transferring them. In order to continue ventures without hindrance risk knowledge and management is essential.

What is Risk?

Risk is the chance of loss, a possibility of failure. Peril is the cause of loss and hazard is a condition that increases the risk, the possibility of loss. For example, while driving the risk is of a motor accident. Peril is when another vehicle driving rashly and negligently, causes a collision accident. Hazard is the condition where the driver is without a seatbelt, therefore the possibility of personal loss increases. In real-time, there can be more than one peril acting simultaneously causing the loss and similarly numerous hazards increasing the possibility of the loss and we will learn about it in detail in the section of Causation.

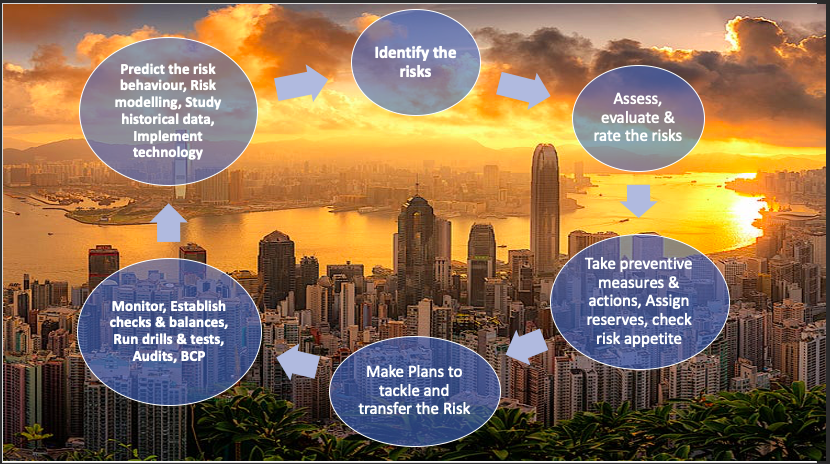

Identification of Risk

Now that we understand the terms, let us proceed with the process of tackling your risk. It is a systematic and logical approach where one first identifies the risk(s).

Identification of risk is an important task and requires diligence. One needs to think of possible factors affecting the venture which may result in a financial loss. For example, a SMEs owner should think of all the perils that may affect the business such as Business premise & content damage, fire, natural calamities & diseases resulting in a pandemic, loss of supply, business interruption, injury to employees, customers, damaged products, theft, burglary, change of laws & regulations and so on. Once these factors are identified we move to the next step.

Assess & Evaluate

One must assess the risks and evaluate the severity along with the costs of making good the damage if the event occurs. Then risk can be rated from least harmful to most harmful, where the latter becomes a priority. Professionals like underwriters and actuaries rate the risk(s) by understanding the various elements that have affected the risk trend in the past and shall affect in coming years due to the changing trends and developments such as technology.

For example damage to motor vehicles due to rain, and flooding has increased worldwide due to climate change, compared to the past 10 years. Logically, you shall find that it is studying the past data of accidental occurrences and their results to predict the chance of suffering a similar or worse outcome. By reflecting on the past incidents that led to the loss one can improvise and take precautions. For example, from studying the past fire accidents in shops the following can be evaluated:

- an average figure of loss suffered (depending on the size of the business, stocks, contents),

- the average figure of salvage possible,

- the common causes of an outbreak such as negligence, shot-circuit, lack of maintenance, and routine checks.

- understand the ways in which the loss could have been avoided such as installing fire extinguishers & alarms, executing routine checks and maintenance, etc. Therefore evaluating and rating the risk is very important to proceed to the next step.

Precaution & Prevention

Once we’re aware of the severity of the risk, we can take precautionary and preventive measures to reduce the impact and be ready with the damage control. We then maintain a financial reserve accordingly for such incidents after evaluation of the loss is complete and have a clearer picture of our loss appetite, i.e. “how much loss can one take on itself?” Taking the above example,

- where fire alarms & extinguishers are installed,

- routine checks are maintained in the log,

- stocks and contents are either kept in a warehouse or protected,

- a security system to monitor and alert,

- fire stations are nearby,

- water sprinklers are installed,

- Insurance policies are in place; It is a step toward managing the risk(s).

Once informed and the preventive measures are in place, tackling the risk has begun. Risk can be tackled by either one or a combination of the below:

- Eliminating the risk altogether. For example, when you know a route has fast-moving heavy vehicles and steep turns, you don’t take it. Further, you stop traveling by car to eliminate any chances of road accidents

- Reducing the risk by having measures in place such as explained above in the fire example.

- Transferring the risk to another entity such as an insurance provider, capital market because they are in the business of risk, with professionals taking care of your profile such as Lloyds of London, Chubbs, Liberty, Axis Capital, etc.

- Retain the risk where supported by your reserves and R&D. If you have the relevant information, you can afford to set aside a reserve.

The idea is to minimize the impact on your venture and maintain continuity. That requires planning ahead with respect to the method or combinations opted for and then focusing on each factor to see what will be required to get back on track. An example would be where the office system is down, the processing and computing can continue on the cloud such as Amazon cloud services provided there exist a backup and recovery plan.

Risk Management

Once tackling plans are in place and you have implemented them the work doesn’t stop. You’re never too careful and there is always scope for improvement and a chance of a mistake. Therefore it is very essential that you formulate a system of risk management in place:

- Routine monitoring of the checks and balances in place

- Routine drills like fire exit drills, physical system switch to cloud drills

- Employ people or guidelines in place to systematically tackle the risk

- Regular and routine audits of processes

- Keep your business continuity plan updated with the changing trends

Further, risk management should be taken seriously, and lately, most organizations have their departments and risk managers in place, however, there are many who need to be aware of this aspect. There are professionals like data scientists who study risk and can predict it by analyzing the historic data and current factors affecting the risk. There are even applications that help in modeling the risk to get possible outcomes.

I hope you understood risk and got an idea on how to manage your risk. Stay tuned to learn interesting stuff like this.