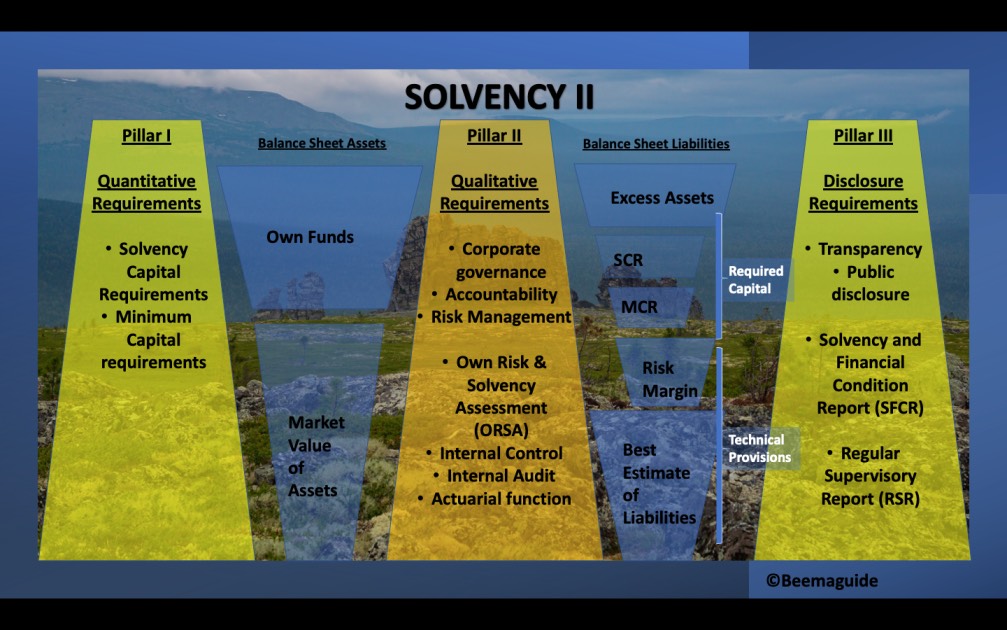

Key takeaway: The 3 pillars of insurance regulation of Solvency II regime.

Introduction

A regime is an orderly way to do things. The solvency II regime was brought to life by the directive 2009/138/EC of the European Parliament on the business of Insurance and Reinsurance in January 2016. It codifies and harmonizes the regulation of insurance in the European Union. It is an effective and sensible framework to:

- Regulate the financial resources,

- Conduct risk assessment and management, and

- Ensure reporting and public disclosure of UK authorized Insurers.

These are the core principles upon which the framework is founded and structured. The essential objective of solvency regulation is:

- To ensure that insurers have reserved adequately for future claims and

- Invested the reserves prudently.

The rationale behind this framework:

- The proliferation of imprudent insurers i.e. weak financial health, poor governance, and reckless investment strategies,

- To prevent imprudent insurers from driving the prudent ones out of the market to the detriment of policyholders,

- To prevent loss of market confidence and from the systemic risk threatening the stability of the insurance sector and financial system.

Solvency II has similarities with the earlier UK Individual Capital Adequacy Standards (ICAS) regime which are:

- Risk-based capital requirements, and

- The use of internal models to calculate the capital requirements.

- Both recognized good governance and strong practices of risk management as key components.

- Solvency II brought in the increased public disclosure of risk capital requirements along with a rule-based detailed legal framework.

The three pillars

Pillar 1

It is all about the measurement of assets, liabilities, and capital. It ensures quantitative (financial resources) requirements where the insurers are required to hold capital so that they can pay claims when insured events occur thus protecting the policyholder. It ensures economic stability by the risk-based approach to its capital resources tailored to specific risks borne by the insurer. An insurer must hold a Minimum Capital Requirement (MCR) which is “eligible basic own funds” sufficient enough to prevent policyholders and beneficiaries from being exposed to an unacceptable level of risk if the insurer continues to carry on its operations.

The confidence level that losses can be absorbed by those own funds over a period must be at least 85%. Calculation and reporting to the supervisory authority are quarterly. Breach of the MCR automatically triggers supervisory action which may include suspension of authorization. The relationship between MCR and SCR falls within a corridor – the MCR must not fall below 25% or exceed 45% of the SCR. Solvency capital requirement (SCR) has to be maintained on top of the MCR, which is calculated either by the standard formula (Arts 101-111) or by a full or partial internal model approved by the relevant supervisory authority (Arts 112-127). SCR requires sufficient own funds to ensure that the insurer will still be in a position, with a probability of 99.5%, to meet obligations to policyholders and beneficiaries at the end of a period.

The SCR is to be reported annually but the requirement to monitor compliance with the SCR is continuous. Assets are to be valued at the amounts for which they could be exchanged between knowledgeable, willing parties in an arm’s length transaction, and liabilities at the amounts at which they could be transferred or settled between such parties (Art 75). The “technical provisions” (TP), required to cover liabilities in respect of business already written, must correspond to the current amount the insurer would have to pay if it were to transfer its obligations immediately to another insurer (Art 76). This is to be calculated as equal to the sum of the best estimate of the probability-weighted average of future cash flows and a risk margin (Art 77). Technical provisions must also include expenses, inflation, and discretionary bonuses to policyholders whether or not they are contractually guaranteed (Art 78).

Pillar 2

It is about quality measures of risks i.e. corporate and risk governance along with own risk and solvency assessment (ORSA) therefore insurers must have in place an effective system of governance that provides for sound and prudent management of their business. It delegates the responsibility upon the board of directors to comply with all Solvency II rules, applicable laws, regulations, and administrative provisions. The system of governance must be proportionate to the nature, scale, and complexity of the insurer’s operations, and must include:

- An adequate transparent organizational structure with a clear allocation and appropriate segregation of responsibilities,

- An effective system for ensuring the transmission of information,

- The risk-management function,

- The internal control (compliance) function,

- The internal audit function, and

- The actuarial function;

- The insurer’s ORSA.

An insurer must ensure that all persons who perform key functions or certification functions are at all times:

- ‘Fit and proper persons’ (i.e. having personal characteristics which show integrity and good reputation),

- Is qualified;

- Possesses the knowledge, experience, and good record).

Insurers must identify and allocate responsibility for key functions and conduct a regular internal review of governance. The risk management system must comprise:

- strategies,

- processes, and

- reporting procedures necessary to identify, measure, monitor, manage and

- report continuously the risks to which it is or could be exposed.

It must be effective and well-integrated into the organizational structure and decision-making processes of the insurers. It must cover the risks to be included in the calculation of the SCR, as well as the risks in the following areas i.e.

- underwriting and reserving;

- asset-liability management;

- investments;

- liquidity risk and

- concentration risk,

- operational risk;

- reinsurance and

- other risk-mitigation techniques.

The risk management function must regularly assess the adequacy of TPs and eligible own funds and investments, and where the internal SCR model is used, take responsibility for design, approval, compliance, etc. The internal control system must include administrative and accounting procedures, appropriate reporting arrangements at all levels, and a compliance function i.e. advising the governing body on compliance with the SII regulations along with an assessment of the possible impact of any changes in the legal environment on the insurer’s operations.

The internal audit function must include an evaluation of the adequacy and effectiveness of the internal control system and other elements of the system of governance. It must be objective and independent of the operational functions. Any findings and recommendations of the internal audit function must be reported to the insurer’s board of directors which then must determine what actions are to be taken for each of the internal audit findings and recommendations and ensure that those actions are carried out.

Insurers must have an effective actuarial function:

- to coordinate the calculation of TP and

- ensure the appropriateness of the methodologies and underlying models used, as well as the assumptions made in the calculation of TP,

- to assess the sufficiency and quality of the data used in the calculation of TP and compare the best estimate against experience,

- to inform the insurer’s board of directors of the reliability and adequacy of the calculation of TP,

- to express an opinion on the overall underwriting policy and on the adequacy of reinsurance arrangements,

- to contribute to the effective implementation of the risk management system, in particular concerning the risk modeling underlying the calculation of the SCR and MCR and to the insurer’s ORSA.

The actuarial function must be carried out by persons who know actuarial and financial mathematics, commensurate with the nature, scale, and complexity of the risks inherent in the insurer’s business, and who can demonstrate their relevant experience with applicable professional and other standards. The OSRA must exhibit:

- the insurer’s overall solvency needs to take into account the specific risk profile, approved risk tolerance limits, and business strategy,

- the compliance must be forward-looking and continuous, with SCR, MCR, and TP;

- the significance with which the risk profile of the insurer deviates from the assumptions underlying the SCR.

Pillar-3

It is all about public disclosure ensuring transparency by making it available to the public periodically either in printed or electronic form free of charge. It must include essential information on their solvency and financial condition. Undertakings should be allowed to disclose publicly additional information voluntarily. An insurer must produce two key reports:

- The Solvency and Financial Condition Report (SFCR) which are required to be reported publicly and annually to the local National Competent Authority;

- The Regular Supervisory Report (RSR) is a private report to the supervisor and is not disclosed publicly. Insurers submit this report to the local National Competent Authority in full at least every three years and in summary every year.

SFCR and RSR include both qualitative and quantitative information. SFCR contains a description of the business and performance of the insurer along with the system of governance of the insurer and an assessment of its adequacy for the risk profile of the insurer. It has the details on the risk exposure, risk concentration, risk mitigation, and risk sensitivity separately for each category of risk of the insurer along with a detailed description, separately for assets, TP, and other liabilities, of the bases and methods used for their valuation, together with an explanation of any major differences in the bases and methods used for the valuation of those assets, technical provisions, and other liabilities in financial statements of the insurer.

It also includes a description of the capital management of the insurer and information showing and explaining the main differences between the underlying assumptions of the standard formula and the underlying assumptions of any internal model for which the insurer has received internal model approval; and the amount of any non-compliance with the MCR or any significant non-compliance with the SCR during the reporting period, even if subsequently resolved, with an explanation of the origin of that non-compliance and its consequences, as well as any remedial measures taken in respect of that non-compliance.

Conclusion

In light of the above, I would conclude that Solvency II is a risk-based approach because of the implementation of a series of quantitative and qualitative measures as described in Pillar 1 and 2. It is open to public scrutiny by the disclosures it has to make as described in its Pillar 3. It is forward-looking because its main intention is to foresee and eradicate any failure and insolvency risk, safeguard and monitor stakeholders from internal and external poor governance by establishing systematic checks and regulating them through reviews, supervisory reporting, and risk management practices and processes. It aims to ensure that insurers have reserved adequately for future claims and invested the reserves prudently. That insurers aim to develop a common approach to solvency regulation and facilitate cross-border cooperation and coordination for the promotion of internal market imperatives. It creates a level playing field for policyholders’ protection and financial stability. Lastly, it promotes legal certainty and predictability ensuring avoidance of regulatory arbitrage.

References

- Solvency II Directive 2009/138/EC

- FSMA 2000

- PRA Rulebook