The London insurance market today runs on electronic claims rails. At the heart of that network sits the Electronic Claims File (ECF2). Understanding how ECF2, CLASS, IMR and the London Market’s key bodies—Lloyd’s, the IUA and DXC—work together is essential for anyone working in London Market claims or operations. This guide takes you through the entire ecosystem step-by-step. Along the way, you’ll find real-world examples and a comprehensive glossary. Even newcomers can follow the full London Market electronic claims journey.

The London Market Claims Ecosystem

The London Market is a specialist, wholesale insurance hub where complex and large commercial risks are placed with multiple insurers on a subscription basis. Understanding the Electronic Claims File (ECF2) in the London Market is critical for claims professionals. Claims in this environment must co-ordinate many parties—policyholders, brokers, Lloyd’s syndicates, company-market insurers, and central service providers—using shared processes and the Electronic Claims File (ECF2) as the central coordination platform.

1.1 Core participants

- Policyholder and local/retail broker: The insured and their local advisor who first spot the loss and notify London.

- London Market broker: Specialist intermediary placing and servicing the London subscription risk, responsible for creating and maintaining the electronic claim.

- Lead and following insurers: Lloyd’s syndicates and/or company‑market insurers subscribing to the risk, with the Lead usually given authority to agree claims under a claims scheme.

- Central services and utilities: DXC (including former Xchanging operations), Velonetic, and market bodies such as Lloyd’s and the IUA provide shared processing, rules and platforms.

Why electronic claims matter

Historically, London Market claims ran on paper files carried around Lime Street. The process was slow, opaque, and prone to data errors. To address these issues, the market introduced ECF and ECF2. These systems standardise and digitise the claim file. Now, all subscribing markets see the same information and agreement status in one place.

With that context in place, it’s important to understand what ECF and ECF2 actually are and how they function in practice.What the Electronic Claims File (ECF) and ECF2 Actually Are

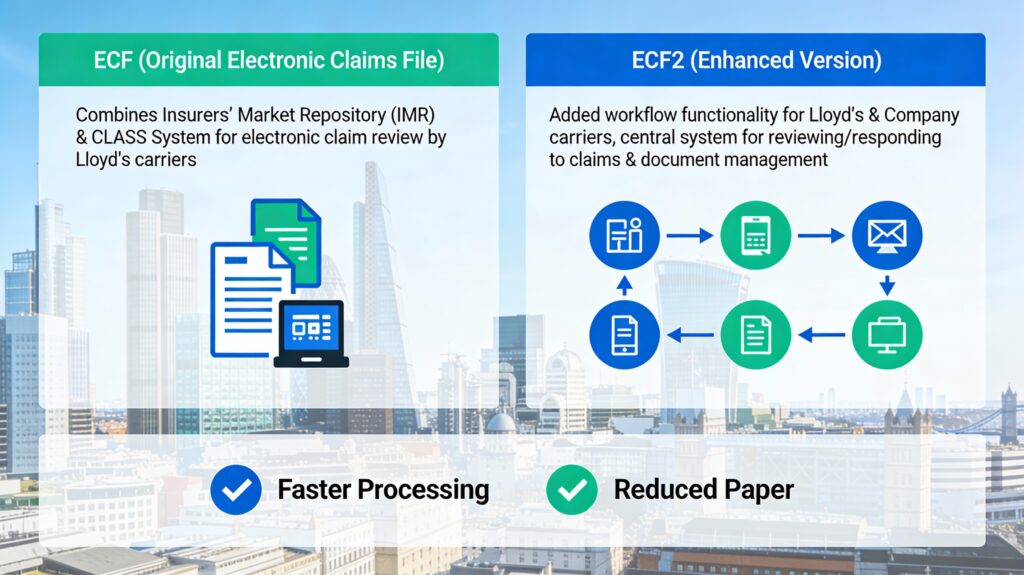

At the foundation of Electronic Claims File (ECF2) in the London Market is a two-layer architecture. ECF is the core electronic claims environment that combines IMR and CLASS. ECF2 is the enhanced modern generation that Lloyd’s and company-market carriers use across the London Market for streamlined claims management. Understanding how these components fit together within the Electronic Claims File (ECF2) ecosystem is the critical first step.

ECF: The basic concept

- ECF (Electronic Claims File) is an integrated service at the core of the Electronic Claims File (ECF2) in the London Market that combines the Insurers’ Market Repository (IMR) and CLASS (Claims Loss Advice and Settlement System) to allow claims to be handled electronically.

- Brokers load claim data into CLASS and documents into the IMR; ECF presents this as a single electronic claim file to insurers, linked via references like UMR and UCR.

Example (market‑style):

A London Market broker handling a global property programme at Lloyd’s creates a claim entry in CLASS, uploads the slip, wording, loss notice and adjuster’s report to the IMR, and ECF then shows a unified claim file to the Lead and following syndicates.

ECF2: The enhanced environment

- ECF2 is the enhanced version of the Electronic Claims File, giving Lloyd’s and IUA carriers a single, central interface to review and respond to claims electronically.

- It adds improved access, workflow components, and integration features such as richer document views, improved agreement screens and workflow triggers.

Key point: ECF2 does not replace CLASS or IMR; it orchestrates and surfaces them more efficiently under one umbrella, whileThis architecture makes Electronic Claims File (ECF2) in the London Market an essential tool for efficient claim processing and agreement management. still relying on those core components.

ECF vs ECF2: Quick Comparison

Below is a quick reference table comparing ECF and ECF2 to help you understand the key differences and improvements between the two versions of Electronic Claims File (ECF2) in the London Market, and how the enhanced Electronic Claims File (ECF2) improves upon the original ECF.

| Aspect | ECF | ECF2 |

|---|---|---|

| Interface | Basic electronic file | Single, central carrier interface |

| User Experience | Manual processes | Improved workflow features |

| Document Access | Linked via references | Richer document views |

| Agreement Screens | Standard | Improved screens |

| Workflow Triggers | Limited | Claims Workflow Triggers (CWT) |

| Integration | Separate systems | More integrated orchestration |

| Adoption | Partial | Full London Market (post-July 2024) |

ECF2 Components And Surrounding Systems in the London Market

IMR – Insurers’ Market Repository

- IMR is the central electronic document repository for the London Market, storing placing and claims documentation.

- Documents are stored at UMR level for placing information and at UCR level for claim‑specific information, and are linked into the ECF claim view.

CLASS – Claims Loss Advice and Settlement System

- CLASS is the system used by brokers to submit claims and subsequent transactions (e.g. advice, settlement, amendment) to the bureau for processing.

- It holds structured data (reserves, claim amounts, dates, parties), which ECF2 uses to drive the electronic claim and which DXC uses to generate bureau accounting and settlement messages.

ECF2 workflow and triggers

- ECF2 exposes claims as “work items” for carriers and produces Claims Workflow Triggers (CWT) that internal carrier systems can consume.

- Standardised events include new claim advices, updates, deletions, completion and changes to agreement responsibilities, allowing carriers’ own workflows to update automatically.

Central processing – DXC and Velonetic

- DXC Technology (incorporating the former Xchanging Ins‑Sure Services and Xchanging Claims Services) delivers core London Market back‑office processing for policies, premiums and claims.

- Velonetic, jointly owned by DXC, Lloyd’s and the IUA, is responsible for the new joint venture platforms that underpin Blueprint Two digital services for premium and claims processing.

Now that you understand the components and systems involved in ECF2, let’s walk through how the Electronic Claims File (ECF2) in the London Market processes a typical claim from notification through settlement. Understanding this Electronic Claims File (ECF2) journey is essential for London Market claims professionals.

This section walks through the typical journey of a subscription open‑market claim using ECF2, drawing on the standard open‑market claims model.

1 – First Notification And Claim Creation

- Policyholder notifies the local/retail broker of a loss (for example, a US manufacturer with a products liability claim).

- The London Market broker gathers details and confirms coverage under the relevant UMR (Unique Market Reference) for the London subscription policy.

- The broker creates a CLASS entry for the claim, generating a UCR (Unique Claims Reference) and populating key data (cause of loss, date, reserves, insured details).

- Placing documents (slip, schedule, wording) are loaded to the IMR at UMR level; claim documents (loss notice, expert reports, correspondence) are loaded at UCR level.

At this point, ECF2 can display a complete electronic claim file, combining CLASS data and IMR documents, ready for insurers to review.

2 – Establishment Of Agreement Parties

- The applicable claims scheme (e.g. Lloyd’s Claims Scheme or SCAP) and the contract determine who the agreement parties are: Lead, second Lead, XCS or additional agreement parties (CAPs).

- ECF2 identifies the relevant agreement parties from the subscription details and presents work items to those parties for response.

In a typical Lloyd’s open‑market risk, the Lead syndicate is the primary CAP empowered to agree or query claims on behalf of followers under the scheme, simplifying the process.

3 – Consideration Of The Claim

- The Lead and any other CAPs access the claim via ECF2 (directly or via internal claim systems consuming CWT messages).

- They review documents, set or adjust case reserves, raise queries with the broker, and record agreement or disagreement to the specific transaction in the claim.

- Queries and responses form an audit trail visible within the electronic file, improving transparency and governance.

Example (real‑world style):

A Lead Lloyd’s marine syndicate reviews a hull damage claim file: surveyor’s report, repair estimates and policy wording are all stored under the UCR in the IMR; the adjuster confirms that the loss is covered subject to deductible and posts “agree – pay 75% of repair cost less deductible” in ECF2.

4 – Bureau Processing Of CLASS Transactions

- Once agreement requirements are satisfied, the broker’s CLASS transaction is processed via DXC’s central services.

- DXC validates data, applies market rules, and generates bureau accounting messages and outputs (such as Underwriters’ Signing Messages, or USM) for the subscribing syndicates and companies.

The integrity of data captured in CLASS and ECF2 is critical here, because it directly drives the financial postings and settlement flows.

5 – Insurer Records And Settlement

- Individual insurer records are updated (often automatically via interfaces using EDI or ACORD‑type messages), and settlements are processed by DXC on behalf of the market.

- Funds move from central settlement accounts to brokers and then to policyholders, closing the chain that began at notification.

For delegated authority or TPA arrangements, bordereaux and loss funds may be involved, but the core principle is the same: ECF2 sits at the centre of the record of agreement for bureau claims.

Behind every ECF2 transaction lies a network of key market bodies that define standards, rules and operational frameworks. Understanding their roles helps explain how ECF2 integrates across the London Market.

Roles Of Key Market Bodies Around ECF2

Lloyd’s

- Lloyd’s provides the framework for the Lloyd’s market, including central oversight, market rules and the Lloyd’s Claims Scheme that underpins Lead/follow claims agreement.

- It works with DXC, Velonetic and the market to deliver the Blueprint Two programme, which changes how central services for premium and claims are delivered and integrated.

IUA – International Underwriting Association

- The IUA represents international and wholesale company‑market insurers in London and is a shareholder in the joint venture delivering new digital services.

- It co‑ordinates with Lloyd’s, LMA and LIIBA on electronic processing, standards and reform initiatives affecting company‑market participants in ECF2 and future platforms.

LMA, LIIBA And LMG

- LMA (Lloyd’s Market Association) represents managing agents and syndicates, including on claims, wordings and market processes.

- LIIBA (London & International Insurance Brokers’ Association) represents London Market brokers, providing input to reforms that affect broker workflows and ECF usage.

- LMG (London Market Group) brings these stakeholder bodies together to drive collective modernisation, notably via the Blueprint Two programme.

Blueprint Two And The Future Of ECF2

Blueprint Two is the London Market’s multi‑year programme to replace legacy central services with modern, data‑driven digital solutions. ECF2 sits alongside this transition and will ultimately interoperate with new back‑office platforms and message standards.

Phase‑one digital services

- From 1 July 2024, all London Market firms have been required to use phase‑one digital services to continue trading, covering premium and claims processing for open‑market and delegated authority business.

- These services introduce new messaging approaches (e.g. ACORD‑based Ebot/Ecot) and a digital gateway that checks that data is complete and fit for straight‑through processing.

Impact on claims handling

- The direction of travel is towards higher data quality, more automation and less manual re‑keying, using ECF2 data and future digital gateways to drive processing.

- Lead/follow models and claims schemes remain central, but the technology under the hood is shifting from legacy EDI towards ACORD standards and API‑style connectivity.

Illustrative Examples Of ECF2 In Practice

The following scenarios show how ECF2 works in practice for different lines of business. These are illustrative but draw on typical London Market structures.

1 Property catastrophe claim

- A global property facultative placement led by a Lloyd’s syndicate and followed by several IUA companies covers a warehouse portfolio.

- A hurricane causes major damage; the local adjuster reports a large loss to the local broker, who passes it to the London broker.

- The London broker:

- Identifies the correct UMR and creates a UCR in CLASS.

- Uploads the slip, wording, schedule, CAT report and adjuster’s preliminary estimate to the IMR.

- ECF2 shows a single claim file to the Lead syndicate and following markets, who review the documentation and agree an initial reserve.

- As the loss develops, the broker submits revised reserve and settlement transactions via CLASS, and ECF2 keeps the running audit trail of all decisions.

2 Casualty (products liability) claim

- A US consumer products manufacturer is insured in London on a subscription basis, with a London broker and a Lloyd’s Lead plus company‑market followers.

- A serious bodily injury claim arises in the US; the local retailer’s claim goes to the manufacturer, who notifies the local broker and ultimately London.

- The London broker loads the claim into CLASS and attaches pleadings, policy wording, coverage counsel opinion and reserves to the IMR.

- The Lead casualty syndicate uses ECF2 to review coverage and quantum, agrees defence cost provisions and later settlement contributions as the litigation proceeds.

3 Delegated authority / TPA arrangements

ECF2 remains the central record of agreement where the claim is processed through the bureau, even though much of the operational handling sits with the TPA.

For delegated authority business (e.g. a US binding authority), a TPA handles day‑to‑day claims, often using a loss fund set up by underwriters.

The TPA pays routine claims and reports on bordereaux; material or complex claims may still be recorded in ECF where bureau processing is needed.

9. Glossary Of Key Terms And Abbreviations

This glossary groups the main abbreviations referenced in this article. Definitions are paraphrased and condensed from recognised London Market sources.

Claims platforms and systems

- ECF – Electronic Claims File

Integrated London Market service for electronic claims handling and processing delivered via the IMR and CLASS, providing a shared electronic claim file for all subscribing insurers. - ECF2 – Electronic Claims File 2

Enhanced version of ECF that allows Lloyd’s and company‑market carriers to review and respond to claims electronically from a single central system, with additional workflow and integration features. - CLASS – Claims Loss Advice and Settlement System

System used primarily by brokers to create and submit claim advices and settlement transactions to bureau processing and to feed data into ECF. - IMR – Insurers’ Market Repository

Central electronic repository storing placing and claims documents at UMR and UCR level, integrated with ECF to provide a complete claim file. - CWT – Claims Workflow Triggers

Structured outputs from ECF2 that signal claim events (new, update, complete, delete, etc.) to carrier workflow systems.

Market references and messages

- UMR – Unique Market Reference

Unique identifier assigned to a London Market contract (often derived from broker and year codes) used to link placements, premiums and claims. - UCR – Unique Claims Reference

Unique identifier for a claim within the bureau systems; all claim transactions for that loss reference the same UCR. - TR – Transaction Reference

Reference identifying an individual premium or claim transaction within bureau processing systems such as CLASS. - USM – Underwriters’ Signing Message

Electronic message used to communicate premium signings and related information to underwriters as part of central processing. - LIMCLM – London Insurance Market Claims Message

Standard electronic format used to transmit claims data across London Market systems.

Market bodies and utilities

- Lloyd’s of London (Lloyd’s)

Insurance and reinsurance marketplace in London made up of syndicates managed by managing agents, providing the platform and rules under which the Lloyd’s market operates. - IUA – International Underwriting Association (of London)

Trade association representing international and wholesale insurance and reinsurance companies in the London Market, particularly the company‑market segment. - LMA – Lloyd’s Market Association

Body representing Lloyd’s managing agents and syndicates, engaged in market initiatives including claims schemes and technical guidance. - LIIBA – London & International Insurance Brokers’ Association

Association representing London Market brokers, involved in market reform, wordings, and process standardisation across placing and claims. - LMG – London Market Group

Market‑wide group that brings together Lloyd’s, LMA, IUA and LIIBA to drive strategic initiatives like Blueprint Two. - DXC – DXC Technology

Global technology company providing London Market central processing services for premium and claims, including operations inherited from Xchanging. - XIS – Xchanging Ins‑Sure Services

Business unit historically responsible for policy and premium processing services for London Market insurers, now part of DXC. - XCS – Xchanging Claims Services

Business unit responsible for central claims processing and related services for the London Market, also now within DXC. - Velonetic

Joint venture owned by DXC, Lloyd’s and the IUA that provides and develops the new central digital services for the London Market, including Blueprint Two platforms. - LIMOSS – London Insurance Market Operations & Strategic Sourcing

Market utility that sources and operates shared services for the London Market and maintains resources like the Market Business Glossary.

Messaging and standards

- EDI – Electronic Data Interchange

Structured method of exchanging business documents electronically between systems in a standardised format, widely used in legacy London Market processing. - ACORD / Ebot / Ecot

ACORD is a global standards body whose messaging frameworks underpin modern London Market back‑office transaction (Ebot) and electronic claims office transaction (Ecot) messages used in Blueprint Two.

Claims schemes and frameworks

- Lloyd’s Claims Scheme

Framework that sets out how claims are to be handled and agreed in the Lloyd’s market, including Lead/follow arrangements and CAP roles. - SCAP – Single Claims Agreement Party

Protocol that allows a single nominated insurer to agree claims on behalf of all subscribing insurers on certain subscription risks, simplifying agreement. - MORF – Market Operational Resilience Framework

Framework describing how the market manages operational disruptions, including procedures for claims handling when ECF2 or other systems are unavailable. - Blueprint Two

Lloyd’s and the wider London Market’s programme to modernise central processing by introducing new digital services, data standards and connectivity for premium and claims.

References (Key Public Sources)

Paraphrased information in this article draws on the following public, London‑Market‑relevant sources:

- ECF information site and glossary for ECF, IMR, CLASS, UMR, UCR and related terms.

- London Market training glossaries for definitions of ECF, CLASS, IMR, EDI and other technical terms.

- Lloyd’s open‑market claims journey and systems, processes and procedures documents for the claims stages and central processing roles.

- DXC and Velonetic materials for descriptions of central services and Blueprint Two digital services.

- London Market Group and IUA information for background on market structure, roles and reform initiatives.

- Additional commentary on London Market claims ecosystem and examples of the core claims journey.

This article has been written in original wording, with care taken to avoid reproducing source text, while maintaining factual accuracy with citations for all technical statements.